AI industry analysis is tricky right now because the market moves fast, vendor claims sound similar, and one quarter of “breakthroughs” can turn into the next quarter’s cost-cutting memo.

If you’re leading strategy, product, or procurement in the US, you usually need three things at once: a read on artificial intelligence market trends, a realistic sense of what you can ship this year, and a way to defend spend decisions when finance asks “what’s the ROI timeline?”

This piece gives you a practical framework: how to interpret market signals, how to map adoption by industry, what to watch in regulation, and how to compare vendors without getting trapped in feature checklists.

How to read AI market signals without chasing hype

A solid AI industry analysis starts with separating “what’s possible” from “what’s purchasable” and “what’s deployable.” Generative demos can be real, but production outcomes depend on data access, risk tolerance, and integration effort.

When you scan news or analyst notes, look for signals that are hard to fake:

- Budget line items: cloud commits, data platform upgrades, security tooling, model monitoring.

- Org changes: AI governance councils, model risk roles, legal review lanes.

- Time-to-value talk: pilots that move into operational KPIs, not just prototypes.

According to OECD guidance on AI policy and measurement, adoption and impact often vary by sector and firm capabilities, so broad headlines rarely translate 1:1 into your plan.

AI market size forecast: what’s useful vs what’s just a big number

Most teams ask for an AI market size forecast to justify investment. The catch: market sizing can be directional but not decision-grade, because definitions differ (AI software vs AI-enabled services vs chips, and now “genAI add-ons”).

Instead of arguing over the “right” number, use forecasts in a more operational way:

- Scenario planning: conservative, base, aggressive assumptions for adoption and pricing.

- Category split: infrastructure, model/API spend, apps, services, internal build.

- Constraint tracking: compute availability, data readiness, security review time.

According to Gartner research commentary on emerging tech adoption patterns, early-stage markets often show uneven value capture, so budgeting should expect variability across use cases and business units.

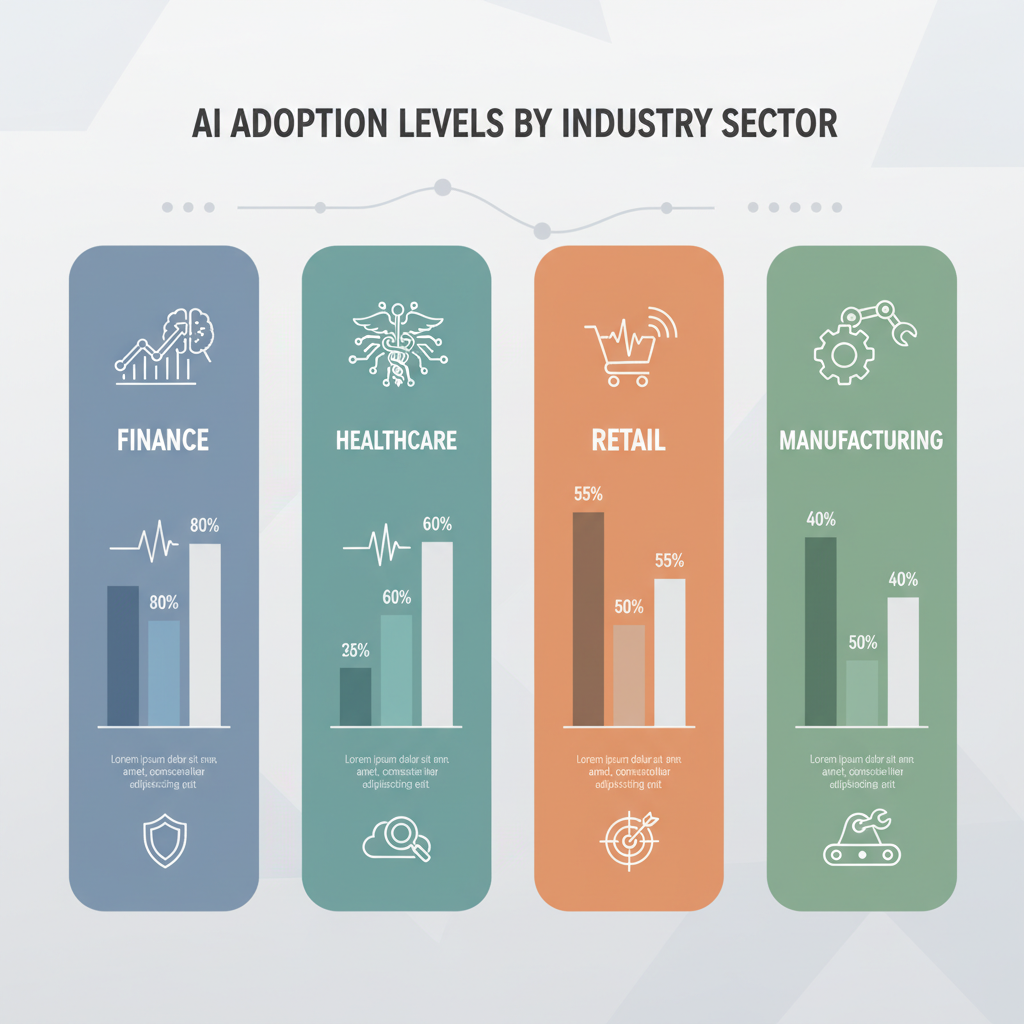

AI adoption by industry: where it tends to stick (and where it stalls)

“AI adoption by industry” sounds like a leaderboard, but reality looks more like a patchwork. Many organizations run AI in one function while other teams stay cautious for good reasons.

Patterns you’ll often see:

- Financial services: strong in fraud, risk analytics, customer service automation, heavy governance.

- Healthcare: promising in documentation and imaging support, slower in high-stakes automation due to compliance and safety review.

- Retail and e-commerce: personalization, demand forecasting, catalog enrichment, pricing experiments.

- Manufacturing: predictive maintenance, visual inspection, supply planning, usually tied to edge constraints.

- Public sector: document workflows and citizen services, with tighter procurement and transparency needs.

If your company struggles to move from pilot to production, it’s often not a “model quality” issue, it’s workflow ownership, data permissions, or unclear accountability when outputs go wrong.

Generative AI market outlook: what changes, what stays the same

The generative AI market outlook has two simultaneous truths: capability improves quickly, and business adoption still bottlenecks around trust, cost, and integration. That tension is why “AI everywhere” can coexist with slow enterprise rollouts.

Three changes that matter for the next planning cycle:

- From chat to workflow: genAI moves into ticketing, CRM, IDEs, contact centers, and knowledge bases.

- Model choice becomes a portfolio: teams mix frontier models, smaller tuned models, and retrieval systems.

- Cost visibility rises: token spend, GPU utilization, and engineering time become CFO-level topics.

What stays the same: companies that win tend to treat AI as product engineering plus change management, not as a one-time tool purchase.

AI competitive landscape: how to compare vendors without getting lost

The AI competitive landscape is crowded: hyperscalers, model providers, MLOps platforms, data vendors, and a long list of app-layer tools. Comparing everything at once usually creates noise.

A practical approach is to decide which “layer” you are buying, then score vendors in that lane. Here’s a lightweight AI vendor comparison matrix you can adapt.

AI vendor comparison matrix (editable starting point)

| Criteria | Why it matters | What to ask |

|---|---|---|

| Data integration | Most value depends on your data access | Connectors, VPC options, on-prem/edge support |

| Security & compliance | Controls determine what you can deploy | Audit logs, encryption, SOC 2 posture, retention controls |

| Model governance | Prevents silent drift and policy violations | Monitoring, evals, red-teaming support, approvals |

| Reliability & SLAs | Downtime breaks business workflows | Latency, uptime, incident process, support tiers |

| Unit economics | Costs can spike with usage | Pricing granularity, caps, caching, volume discounts |

| Build vs buy fit | Determines team workload and speed | APIs, SDKs, customization limits, portability |

According to NIST publications on AI risk management, governance and measurement should be planned early, which is another way of saying vendor selection is also a risk decision, not only a feature decision.

AI pricing and monetization models: the part most forecasts ignore

Even a strong AI industry analysis can fail if the pricing model doesn’t match usage reality. Many teams underestimate cost volatility, especially with generative workloads.

Common AI pricing and monetization models you’ll run into:

- Usage-based: tokens, calls, GPU time, pages processed. Flexible, but can surprise you.

- Seat-based: easier budgeting, sometimes mismatched to heavy users.

- Outcome-based: appealing, but definitions can get contentious.

- Platform bundles: “AI included,” with limits hidden in rate caps or premium tiers.

Cost controls that actually help in practice:

- Routing: send simple tasks to cheaper models, reserve premium models for hard cases.

- Caching and retrieval: reduce repeated generation, ground answers in your content.

- Evaluation gates: stop bad outputs before they hit customers or agents.

AI regulation impact assessment: what to watch in the US

An AI regulation impact assessment is less about predicting one law and more about designing for scrutiny. In the US, requirements can vary by state, sector, and procurement rules, and many companies also align with global expectations to avoid rework.

According to The White House guidance on AI (including executive actions and policy frameworks), organizations are encouraged to emphasize safety, security, and responsible use, especially for high-impact domains.

For planning, focus on controls that are useful even if rules change:

- Data provenance: where training or reference data comes from, what rights you have.

- Human oversight: clear escalation paths for sensitive decisions.

- Documentation: model cards, decision logs, evaluation results.

- Risk tiering: classify use cases by impact, apply stricter review where needed.

If you operate in regulated areas (health, finance, employment), it’s usually smart to involve counsel and compliance early, rather than retrofit controls after a rollout.

Practical benchmarking: picking use cases that survive the pilot phase

If you’re doing AI use case benchmarking, the goal is not “the most innovative idea,” it’s the use case with a clear owner, measurable throughput, and acceptable risk. That’s what survives contact with production.

A quick self-check (5 minutes)

- Is there a single business owner who benefits and will fund phase two?

- Is the input data accessible without months of permissions work?

- Can you define a quality metric beyond “looks good”?

- Do you have a fallback path when the model is uncertain?

- Is the workflow high-frequency enough to matter financially?

Step-by-step rollout (what tends to work)

- Start narrow: one team, one workflow, one measurable KPI.

- Instrument early: log prompts, inputs, outputs, user actions, and cost signals.

- Run evals continuously: spot regressions, drift, and policy violations.

- Scale with guardrails: expand access as reliability and governance mature.

When you need an AI investment and funding analysis, bring this rollout plan to finance. It turns “AI spend” into staged risk reduction, which is usually an easier conversation.

Key takeaways (keep this handy)

- Use forecasts for scenarios, not as a single-number truth.

- Adoption is uneven and often blocked by data access and governance, not model accuracy.

- Vendor comparison works best by layer, with unit economics and controls in the scorecard.

- Regulation readiness is a design choice: documentation, oversight, and risk tiering pay off.

Conclusion: turn analysis into a decision, not a document

A good AI industry analysis should leave you with fewer options, not more. Once you pick a lane, keep your comparison criteria tied to risk, cost, and the workflow you’re actually changing.

If you want a simple next step, choose one priority workflow, draft a vendor matrix with cost controls, and run a 6–10 week pilot with instrumentation and clear acceptance criteria. That’s usually enough to reveal whether you’re looking at a real productivity lever or just a compelling demo.